Model Portfolios | April Update

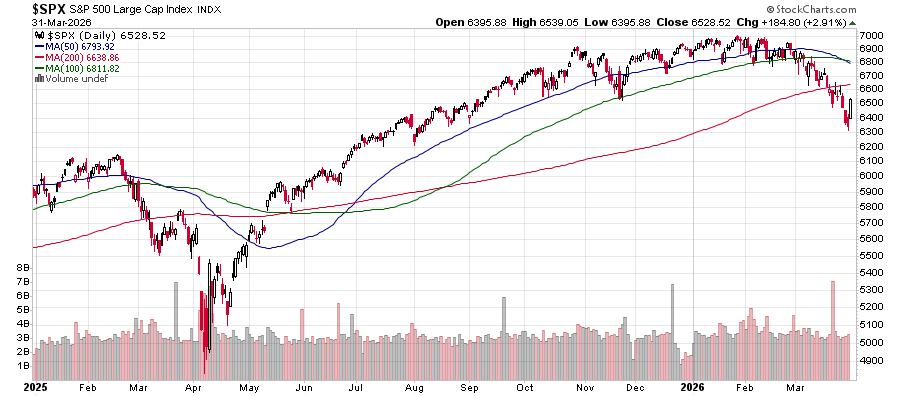

S&P 500 6528.52 | 10-Year UST Yield 4.31% | March 31, 2026

“Investment success doesn’t come from ‘buying good things’, but rather from ‘buying things well’.”

COMMENTARY

Through March 31st, the S&P 500 has declined 6.5% from its all-time high reached on January 27, 2026. It is currently trading around the same level as it did last summer. The selloff has been more severe in the tech-weighted Nasdaq Composite, which has declined 9.9% from its all-time high made five months ago on October 29, 2025. We are well on our way toward identifying an attractive stock market buying opportunity later this year. Last month, we noted the “primary reason the S&P 500 has been unable to advance since October is the exhaustion of upside momentum in large-cap technology stocks.” That remains the case, despite the excitement about a productivity surge driven by broad AI adoption.

Investors are increasingly concerned about an economic slowdown and rising inflationary pressures. The New York Fed’s GDP Nowcast estimates first-quarter real GDP growth at +2.1%, while the Atlanta Fed’s GDPNow forecasts 2.0% growth in the first quarter. In the fourth quarter of 2025, real GDP growth slipped to 0.7%, following 4.4% growth in the third quarter.

Subscriber Note: We added an “Economic Dashboard” to our website, which tracks the key economic indicators we regularly monitor. You can access it anytime here: https://econ.brinkeradvisor.com/

The Association of American Railroads (AAR) reported that total combined rail traffic increased 1.8% through the first 11 weeks of 2026 compared to the same period last year. The combined rail traffic figure includes cumulative carload volume up 4.7% and intermodal units down 0.4%. In the most recent reporting week, five of the ten carload commodity groups posted increases compared to the same week last year, while the remaining five posted declines.

The American Trucking Associations’ Truck Tonnage Index rose 2.6% in February, following a 0.7% increase in January, rising to the highest level in 3 years. On a year-over-year basis, the index rose 2.1%, the largest year-over-year gain since October 2022. Trucking is an excellent barometer of economic activity, accounting for more than 70% of the tonnage carried by all modes of domestic freight transportation. A recovery in the goods sector appears to be underway.

The American Staffing Association (ASA) Staffing Index suggests staffing trends are holding steady. The index’s four-week moving average was unchanged at 86. Temporary and contract staffing employment in the four weeks ending March 15 was 4.0% higher than in the same period of 2025. We follow temporary staffing levels because short-term staffing changes often precede changes in full-time staffing.

HOUSING MARKET UPDATE

The NAHB/Wells Fargo Housing Market Index (HMI) measures conditions in the single-family housing market. The index rose one point in March to 38, well below the 50 threshold that signals favorable sentiment among builders. The current sales conditions index increased one point to 42; the measure of sales expectations over the next 6 months gained two points to 49; and the prospective buyer traffic index rose three points to 25. The NAHB Chair noted that “affordability for buyers and builders remains a top concern” and that “many buyers remain on the fence waiting for lower interest rates and due to economic uncertainty”. Nearly two-thirds of builders continue to offer sales incentives to support the market. Regionally, the Northeast was static at 44, the Midwest was unchanged at 43, the South held steady at 35, and the West fell two points to 31.

INFLATION UPDATE

The Fed’s preferred inflation measure is the personal consumption expenditures (PCE) price index. In January, the headline PCE inflation rate was 2.8% year-over-year. The core PCE inflation rate, which excludes the volatile food and energy components, was 3.1% year-over-year in January. These inflation figures remain stubbornly above the Fed’s 2% inflation target. More importantly, the recent increase in energy prices worldwide makes it unlikely that we will see inflation move toward the 2% target in the near term. Accelerating inflation makes it challenging for FOMC members to lower the fed funds rate.

Headline PCE:

+0.3% seasonally adjusted

+2.8% year-over-year

Core PCE: (excludes food and energy)

+0.4% seasonally adjusted

+3.1% year-over-year

FEDERAL RESERVE UPDATE

The next FOMC meeting is scheduled for April 28th and 29th. At the March meeting, FOMC members voted 11-1 to keep the fed funds rate unchanged at the 3.5% to 3.75% target range. The Committee also continued its balance sheet policy, noting that it will increase System Open Market Account holdings by purchasing Treasury bills and, if needed, other Treasury securities with remaining maturities of 3 years or less to maintain ample reserves. The Fed will also roll over at auction all principal payments from its Treasury securities holdings and reinvest all principal payments from its agency securities holdings into Treasury bills.

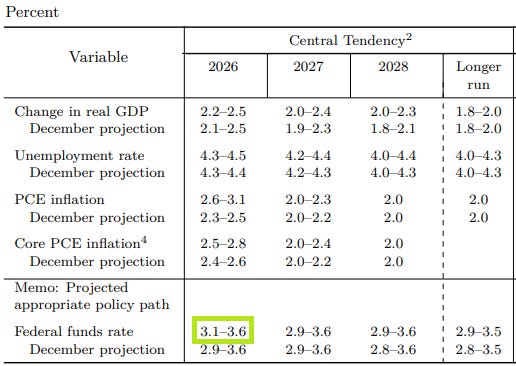

In the March 2026 Summary of Economic Projections, FOMC members left their median forecast for the fed funds rate at year-end 2026 unchanged at 3.4%. The central tendency was in a range of 3.1% to 3.6%, indicating roughly zero to two rate cuts between now and year-end, depending on how the economy and inflation evolve. Compared with the December projections, the central tendency for 2026 real GDP growth edged slightly higher to 2.2% to 2.5%, the unemployment rate forecast was 4.3% to 4.5%, and the PCE inflation forecast increased to 2.6% to 3.1%.

The next FOMC meeting is a month away, but as of this writing, most FOMC members are content to leave the fed funds rate unchanged, waiting to see how the economic data evolves over the coming months.

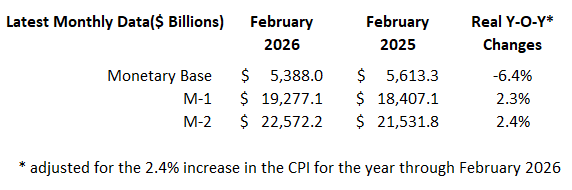

MONEY SUPPLY

MODEL PORTFOLIOS UPDATE

Below is the monthly update of the Marketimer and Brinker Fixed Income Advisor Model Portfolios through March 31, 2026.