Model Portfolios | January Update

S&P 500 4,769.83 | 10-Year UST Yield 3.88%

“If you do not take an interest in the affairs of your government, then you are doomed to live under the rule of fools.”

-Plato

COMMENTARY

Happy New Year! 2023 was a good year for investors as stocks, bonds, and cash posted attractive total returns. The S&P 500 Index produced a total return of 26.3%, including dividends. The S&P U.S. Aggregate Bond Index increased 5.8%. Our preferred cash vehicle, the Vanguard Federal Money Market Fund (Symbol: VMFXX), returned 5.1%.

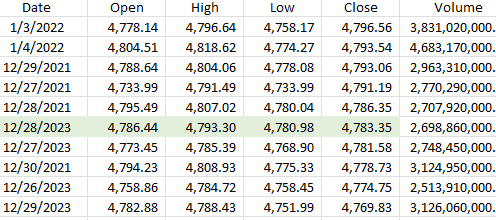

The S&P 500 is approaching a new all-time closing high, ending 2023 about one-half percent below the record high of 4,796.56. The 2023 closing high was 4,783.35 on December 28th. The table below shows the top ten highest S&P 500 Index closing levels:

Our 2024 forecast is for real GDP growth within a range of 1% to 2%, a deceleration in the pace of inflation to the Fed's 2% target level, and a weakening labor market. The Fed is expected to begin lowering the fed funds rate in the first half of 2024, possibly as early as March.

The Fed’s preferred inflation measure is the personal consumption expenditures (PCE) price index. In November, the headline PCE inflation rate was 2.64% year-over-year, well below its peak of 7.1% in June 2022. The core PCE inflation rate, which excludes the volatile food and energy components, was 3.15% year-over-year in November, down from its peak level of 5.6% in February 2022. The most recent three-month core PCE rate is 2.16% annualized, and the six-month core PCE rate is 1.87% annualized. The three-month and six-month core inflation rates are hitting the Fed’s 2.0% inflation target.

The NAHB/Wells Fargo Housing Market Index (HMI) increased by three points to 37 in December, halting a four-month downturn. This rebound was primarily driven by the decrease in longer-term interest rates, leading to a roughly 50 basis point drop in mortgage rates and attracting more prospective buyers. The HMI's future sales expectations component also saw a six-point rise in December. Home builders are actively employing strategies such as price reductions and sales incentives to draw in buyers. The HMI prospective buyer traffic component increased by three points, while the six-month sales expectations component climbed by six points. The current sales conditions component was unchanged.

FEDERAL OPEN MARKET COMMITTEE

The Federal Open Market Committee (FOMC) is scheduled to meet on January 30th and 31st. We do not anticipate any change to the federal funds rate at the January meeting. We expect the Fed’s quantitative tightening program will continue for now; however, we believe the Fed will wind down the program later this year. The Fed’s Summary of Economic Projections forecasts a series of rate cuts in 2024, and investors agree that roughly 100 to 150 basis points of rate cuts are likely throughout the year.

MONEY SUPPLY

U.S. TREASURY RATES

Below is the monthly update of the Marketimer Model Portfolios and the Brinker Fixed Income Advisor Model Portfolios through December 31, 2023.