Model Portfolios | June Update

S&P 500 7580.06 | 10-Year UST Yield 4.45% | May 31, 2026

“Nothing sedates rationality like large doses of effortless money.”

COMMENTARY

The S&P 500 closed at a record high of 7580.06 on May 29, up 10.7% year-to-date. Gains in AI-related technology shares continue to have an outsized impact on market-cap-weighted indices. By our classification, the ten largest stocks represent roughly 40% of the S&P 500, while semiconductor and semiconductor equipment companies represent roughly 17%.

Consensus earnings estimates have become unusually optimistic, with analysts projecting S&P 500 earnings growth of more than 20% over the coming quarters, near the top of the historical range. According to Goldman Sachs research, one company, Micron, accounts for more than half of the S&P 500 earnings revisions since the end of January. Applying the trailing four-quarter operating earnings of about $265 through Q1 2026, the S&P 500 trades at 28.6 times reported earnings. The index has rarely traded at this valuation level outside periods when earnings were temporarily distorted or speculation was extreme.

FINRA data show that debit balances in customers’ securities margin accounts reached a nominal record $1.304 trillion in April 2026, up 53.3% from a year earlier. Since FINRA’s historical margin series began in January 1997, year-over-year increases of this magnitude have occurred in only a few prior episodes, most notably the late-1999/early-2000 dot-com period. Traditional margin debt also understates total speculative leverage because it does not capture leverage embedded in the options market, particularly the surge in 0DTE (zero days to expiration) options.

Household equity exposure also remains unusually high. In the latest Fed Financial Accounts data, the household/nonprofit sector held a record 47.1% of financial assets in directly and indirectly held corporate equities. Using a narrower liquid-asset denominator—deposits and money-market funds, debt securities, and equities—equities represented roughly two-thirds of liquid household financial assets in Q4 2025. Historically, similar periods of equity exposure led to weak real stock market returns.

HOUSING MARKET UPDATE

The NAHB/Wells Fargo Housing Market Index (HMI) measures conditions in the single-family housing market. The index increased three points in May to 37, but it remains well below the 50 threshold that signals favorable sentiment among builders. The latest figure is consistent with a soft single-family housing market.

The latest HMI survey also showed that 32% of builders cut prices in May, down from 36% in April. The average price reduction was 6%, up from 5% in April. The use of sales incentives was 61% in May, up slightly from 60% in April, marking the 14th consecutive month in which this share has reached 60% or higher.

All three major HMI components posted gains in May. The current sales conditions index rose three points to 40; the measure of sales expectations over the next six months increased three points to 45; and the prospective buyer traffic index gained three points to 25. The NAHB noted that the housing market remains under pressure from higher mortgage rates, rising costs, and broad affordability challenges, even though some buyers moved ahead during the spring selling season.

Regionally, the Midwest rose one point to 43, the Northeast rose one point to 42, the South held steady at 35, and the West fell one point to 28.

The supply of new homes available for sale remains highly elevated and is approaching prior peak levels. At the peak of the housing crisis, months’ supply of new homes reached roughly 12.2 months in January 2009. In April 2026, months’ supply rose to 9.4 months, up from 8.7 months in March and well above the normal range of roughly 4 to 6 months.

INFLATION UPDATE

The Fed’s preferred inflation measure is the personal consumption expenditures (PCE) price index. In April, the headline PCE inflation rate rose 3.8% year-over-year, while the core PCE inflation rate, which excludes the volatile food and energy components, rose 3.3% year-over-year. On a monthly basis, headline PCE increased 0.4%, while core PCE increased 0.2%. These inflation figures remain well above the Fed’s 2% target. More importantly, the year-over-year readings show little evidence that inflation is moving sustainably back toward 2%, making it difficult for the Fed to lower the fed funds rate.

Headline PCE:

+0.4% seasonally adjusted

+3.8% year-over-year

Core PCE:

+0.2% seasonally adjusted

+3.3% year-over-year

FEDERAL RESERVE UPDATE

Fed Chair Kevin Warsh took office on May 22 to serve a four-year term. Chair Warsh has been a vocal critic of Fed policies in recent years, so investors will watch closely to see what changes, if any, he pursues. A few ideas he has discussed publicly include reducing the number of FOMC communications about future monetary policy decisions and reducing the size and scope of the Fed’s $6.7 trillion balance sheet. Warsh faces a complicated inflation outlook, with oil prices remaining volatile following disruptions to ship traffic in the Strait of Hormuz.

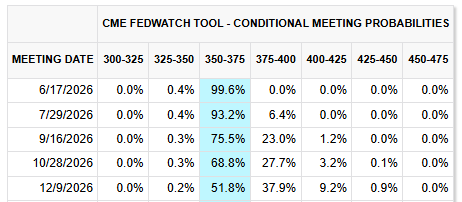

The next FOMC meeting is scheduled for June 16-17. The meeting will include an updated Summary of Economic Projections (SEP) from FOMC members. The March 2026 projections are available here. We do not anticipate any monetary policy change at the June meeting. CME FedWatch shows a 99.6% probability of no change to the fed funds rate in June and a 93.2% probability of no change in July.

MONEY SUPPLY

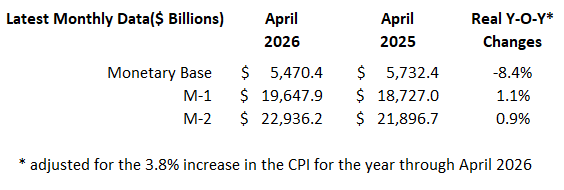

On an inflation-adjusted basis, the monetary base was down 8.4% year-over-year through April, while real M-1 and real M-2 were up 1.1% and 0.9%, respectively. These figures suggest that broad real money growth remains subdued.

MODEL PORTFOLIOS UPDATE

Below is the monthly update of the Marketimer and Brinker Fixed Income Advisor Model Portfolios through May 31, 2026.

{kind=link}