Model Portfolios | March Update

S&P 500 6878.88 | 10-Year UST Yield 3.95% | March 1, 2026

“History does in a vague way repeat itself, but it does it slowly and ponderously, and with an infinite number of surprising variations.”

COMMENTARY

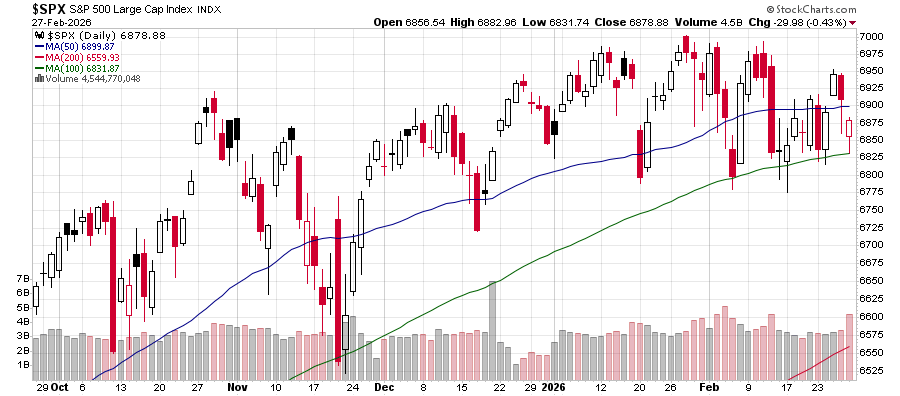

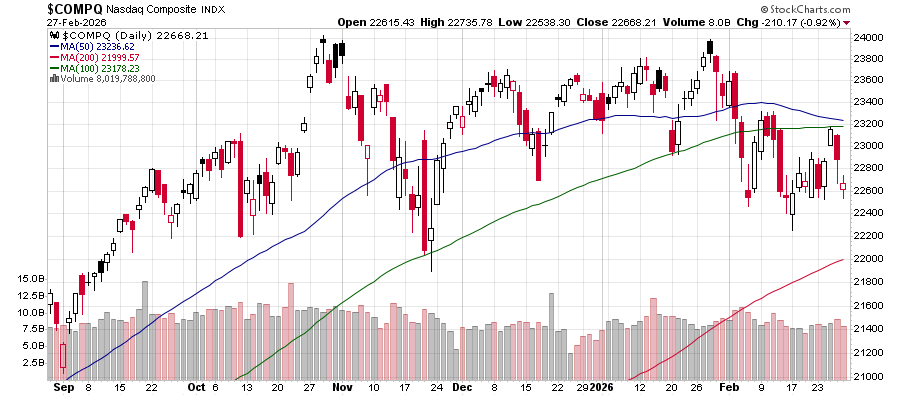

The S&P 500 has been moving sideways over the past four months. In February, it closed at 6879, slightly below its closing level of 6891 reached on October 28th. The primary reason the S&P 500 has been unable to advance since October is the exhaustion of upside momentum in large-cap technology stocks. The Nasdaq Composite index achieved its all-time closing high of 23958 on October 29th. Every subsequent Nasdaq rally since late October has failed. The tech-heavy Nasdaq finished February at roughly the same levels it was trading at in September. (See Nasdaq chart below)

We have mentioned before that the largest technology companies now represent a significant 40% weighting in the S&P 500 Index. We think it is unlikely equity markets will be able to make a sustainable move higher without the participation of large-cap technology stocks.

Investors continue to add leverage to their investment accounts. FINRA reported that investors’ margin debt balances reached another record high of $1.3 trillion in January, up 36.5% year-over-year. Regardless of when the market turns lower, this increasing level of margin debt will accelerate the pace of the decline as leveraged investors are forced to sell. In addition, short-dated options volume continues to grow according to CME Group. “Interest in short-dated options has grown, with maturities under one week now driving a large portion of overall Equity option trading volumes.”

Money Market Assets climbed to $7.8 trillion in late February, including $3.1 trillion in retail accounts. Below is a note we published last week that lists some of the most attractive CD rates available nationwide:

HOUSING MARKET UPDATE

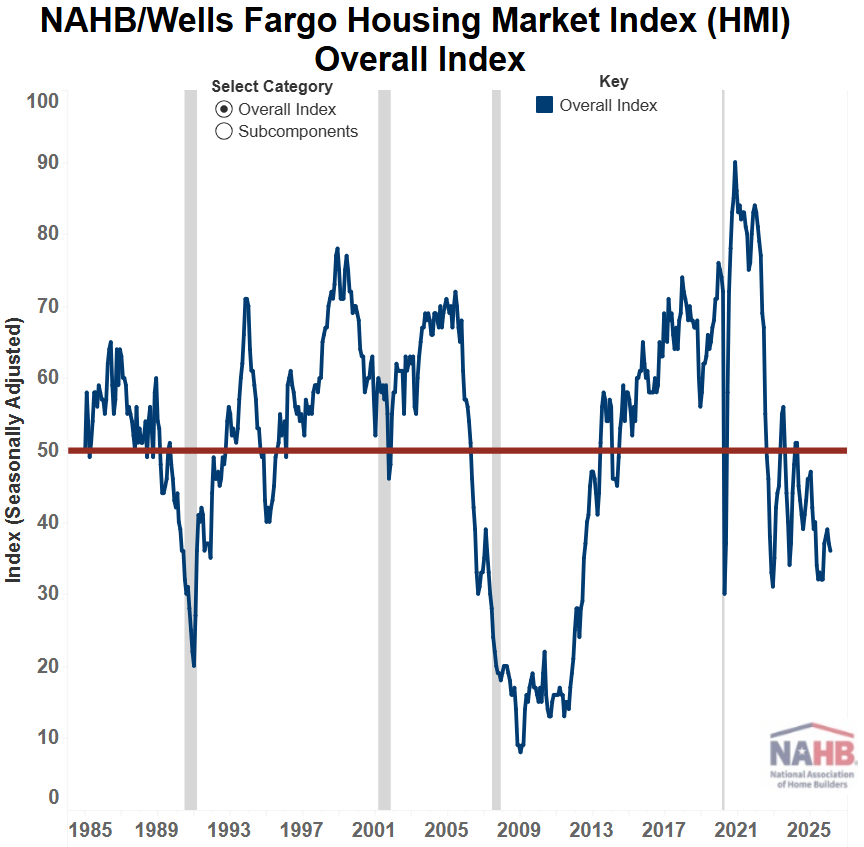

The NAHB/Wells Fargo Housing Market Index (HMI) measures conditions in the single-family housing market. The index fell one point in February to 36, well below the 50 threshold that signals favorable sentiment among builders. The current sales conditions index was unchanged at 41; the measure of sales expectations over the next 6 months fell by three points to 46; and the prospective buyer traffic index dropped by two points to 22. The NAHB Chair noted that “the majority of builders continue to deploy buyer incentives, including price cuts, many prospective buyers remain on the sidelines. Although demand for new construction has weakened, remodeling demand has remained solid given a lack of household mobility.” Regionally, the Northeast fell one point to 43, the Midwest was unchanged at 43, the South fell one point to 35, and the West dropped two points to 33.

INFLATION UPDATE

The Fed’s preferred inflation measure is the personal consumption expenditures (PCE) price index. In December, the headline PCE inflation rate was 2.9% year-over-year. The core PCE inflation rate, which excludes the volatile food and energy components, was 3.0% year-over-year in December. These inflation figures remain stubbornly above the Fed’s 2% inflation target. More importantly, there is little evidence that the inflation rate is moving toward the 2% target, making it difficult for the Fed to lower the fed funds rate despite signs of a weak labor market.

Headline PCE:

+0.4% seasonally adjusted

+2.9% year-over-year

Core PCE: (excludes food and energy)

+0.4% seasonally adjusted

+3.0% year-over-year

FEDERAL RESERVE UPDATE

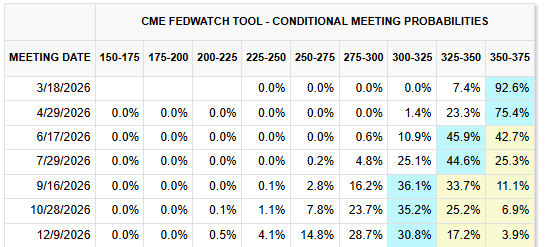

The next FOMC Meeting is scheduled for March 17th and 18th. The meeting will include an updated Summary of Economic Projections (SEP) from FOMC members. Here is a link to their December 2025 projections. We do not anticipate any monetary policy change at the March meeting. CME FedWatch probabilities show a 93% expectation of no change to the fed funds rate in March.

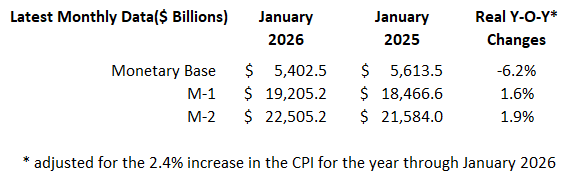

MONEY SUPPLY

The inflation-adjusted year-over-year growth rate of the monetary base stands at -6.2% through January, while the growth rates of M-1 and M-2 are 1.6% and 1.9%, respectively.

MODEL PORTFOLIOS UPDATE

Below is the monthly update of the Marketimer and Brinker Fixed Income Advisor Model Portfolios through February 28, 2026.