Model Portfolios | May Update

S&P 500 7209.01 | 10-Year UST Yield 4.39% | April 30, 2026

“We're blind to our blindness. We have very little idea of how little we know.”

COMMENTARY

The S&P 500 rallied sharply in April, reaching new record highs. Gains in AI-related technology shares fueled the rally. By our calculations, the market-cap weight of semiconductor companies has increased from less than 5% to roughly 15% of the S&P 500’s market capitalization in recent years. Earnings estimates have moved higher, with blended first-quarter earnings growth exceeding 15%. Based on our updated 2026 calendar-year earnings estimate of $295, the S&P 500 is again trading at 24x forward earnings.

Real gross domestic product (GDP) grew at a 2.0% annual rate in the first quarter of 2026, following a 0.5% pace of growth in the fourth quarter, according to the latest Bureau of Economic Analysis report. During the most recent six-month period ending March 2026, real GDP grew at an average annualized pace of 1.25%.

Personal consumption expenditures (consumer spending) are the most significant component within the GDP report, accounting for nearly 70% of GDP. During the first quarter, personal consumption expenditures contributed 1.1 percentage points to the 2.0% GDP increase, as consumer spending decelerated from the prior quarter. Gross private domestic investment contributed about 1.5 percentage points, net exports subtracted about 1.3 percentage points, and government spending added about 0.7 percentage points. View a more detailed GDP contribution breakdown in Table 1.5.2 of the report here.

Looking ahead, the Atlanta Fed’s initial GDPNow estimate for second-quarter GDP growth was 3.7% on April 30, while the New York Fed Staff Nowcast stood at 2.8% for Q2 in its latest posted weekly update.

Subscriber Note: We recently added an “Economic Dashboard” to our website, which tracks the key economic indicators we regularly monitor. You can access it anytime here: https://econ.brinkeradvisor.com/

HOUSING MARKET UPDATE

The NAHB/Wells Fargo Housing Market Index (HMI) measures conditions in the single-family housing market. The index fell four points in April to 34, well below the 50 threshold that signals favorable sentiment among builders. The current sales conditions index fell four points to 37; the measure of sales expectations over the next six months dropped seven points to 42; and the prospective buyer traffic index declined three points to 22. The NAHB Chair noted that “builder sentiment has fallen back in spring as buyers face ongoing elevated interest rates and growing economic uncertainty.” Sixty percent of builders continue to offer sales incentives to support the market. Regionally, the Northeast fell two points to 42, the Midwest dropped two points to 41, the South held steady at 35, and the West fell three points to 29.

INFLATION UPDATE

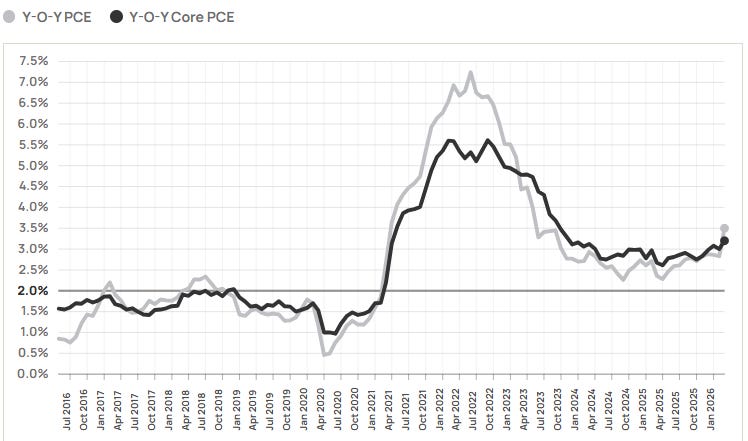

The Fed’s preferred inflation measure is the personal consumption expenditures (PCE) price index. In March, the headline PCE inflation rate was 3.5% year-over-year. The core PCE inflation rate, which excludes the volatile food and energy components, was 3.2% year-over-year in March. These inflation figures remain stubbornly above the Fed’s 2% inflation target. We expect headline inflation to rise in the coming months if elevated energy costs persist, making it more difficult for FOMC members to justify a near-term reduction in the federal funds rate.

Headline PCE:

+0.7% seasonally adjusted

+3.5% year-over-year

Core PCE: (excludes food and energy)

+0.3% seasonally adjusted

+3.2% year-over-year

FEDERAL RESERVE UPDATE

The next FOMC meeting is scheduled for June 16-17 and will include an updated Summary of Economic Projections. At the April meeting, the FOMC voted 8-4 to approve the monetary policy action, maintaining the federal funds target range at 3.50% to 3.75%. The vote was the most divided FOMC decision since 1992. Fed Governor Stephen Miran dissented in favor of a 25-basis-point rate cut. At the same time, Fed Presidents Beth Hammack, Neel Kashkari, and Lorie Logan supported holding rates steady but objected to retaining an easing bias in the policy statement.

The Senate Banking Committee advanced Fed Chair nominee Kevin Warsh in a 13-11 vote on April 29. Reuters reported that the full Senate is expected to vote on Warsh’s confirmation during the week of May 11. If confirmed on that timeline, Warsh could assume the chair role around May 15, when Powell’s term as Fed Chair ends. Gov. Miran’s term expired in January, and Warsh will replace his open seat on the seven-member Fed Board of Governors. During his post-meeting press conference, Chair Powell said he plans to remain on the Board as a governor for an undetermined period after his term as chair ends, as he awaits a resolution to a few ongoing legal cases. Chair Powell’s term as Fed Governor runs into January 2028.

Below is the full monetary policy statement following the April FOMC meeting:

Recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have remained low, on average, and the unemployment rate has been little changed in recent months. Inflation is elevated, in part reflecting the recent increase in global energy prices.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Developments in the Middle East are contributing to a high level of uncertainty about the economic outlook. The Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 3‑1/2 to 3‑3/4 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Philip N. Jefferson; Anna Paulson; and Christopher J. Waller. Voting against this action were Stephen I. Miran, who preferred to lower the target range for the federal funds rate by 1/4 percentage point at this meeting; and Beth M. Hammack, Neel Kashkari, and Lorie K. Logan, who supported maintaining the target range for the federal funds rate but did not support inclusion of an easing bias in the statement at this time.

Below is Chair Powell’s post-meeting press conference: [PDF Transcript]

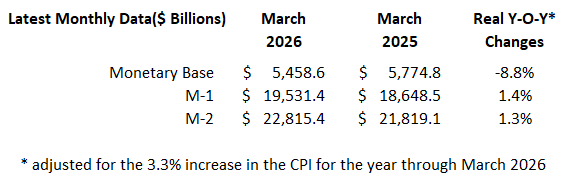

MONEY SUPPLY

MODEL PORTFOLIOS UPDATE

Below is the monthly update of the Marketimer and Brinker Fixed Income Advisor Model Portfolios through April 30, 2026.