Model Portfolios | October Update

S&P 500 5762.48 | 10-Year UST Yield 3.78% | October 1, 2024

“People are trying to be smart - all I am trying to do is not to be idiotic, but it's harder than most people think.”

COMMENTARY

The S&P 500 closed at record-high territory multiple times in September, slightly above the 5667.20 all-time high achieved in July. Long-time readers know that presidential election years are bullish historically, and this year has been a good one for equities, with the S&P 500 up 21% year-to-date through September. Nonetheless, there remains a large and growing amount of money in money market funds, now exceeding $6.4 trillion, including $2.6 trillion in retail accounts per ICI.

Real GDP increased at a 3.0% annual rate in the second quarter, following a 1.6% increase in the first quarter. The latest Atlanta Fed GDPNow estimate is for third-quarter GDP growth of 2.5%, and the New York Fed Staff Nowcast forecasts 3.0% GDP growth. We expect the pace of real GDP growth in calendar year 2024 to be near our long-term 2.0% trend growth rate. This month, we will review our real-time economic indicators.

The Association of American Railroads (AAR) reported US railroads saw total combined rail traffic increase 3.3% through the first 38 weeks of 2024 compared to last year. The combined rail traffic figure includes cumulative carload volume down 3.3% and intermodal units up 9.6%. The decline in carload volume is attributed to the drop in coal volume, which fell 14.7% compared to last year. In the most recent week of reporting, six of the ten carload commodity groups posted an increase compared to the same week last year.

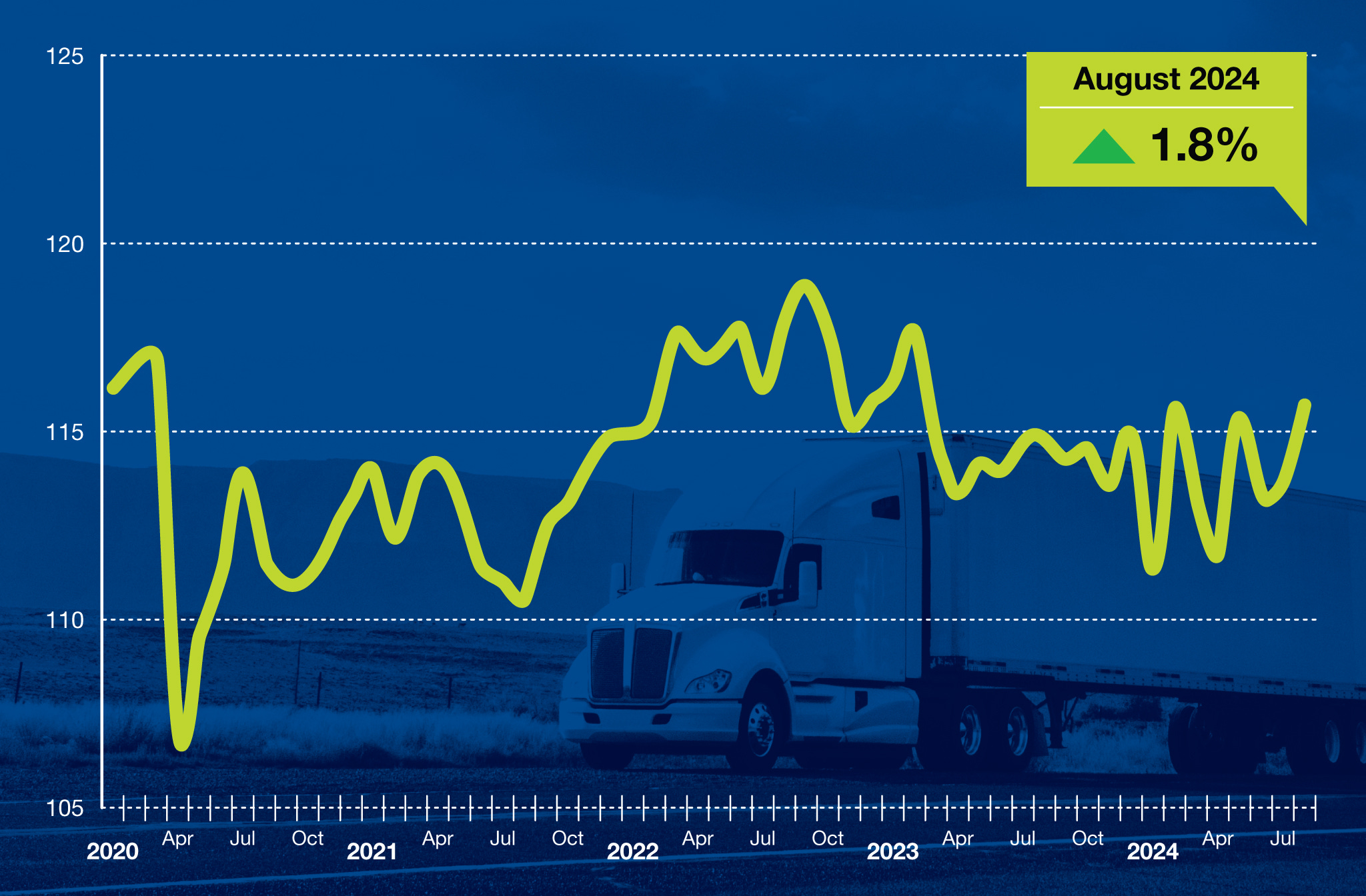

The American Trucking Associations’ Truck Tonnage Index rose 1.8% in August following a 0.4% increase in July. August tonnage rose to the highest level since February 2023. On a year-over-year basis, the index rose 0.7%. Trucking is an excellent barometer of economic activity, representing more than 70% of U.S. goods transported. The recovery in the goods sector appears to be underway.

The American Staffing Association (ASA) Staffing Index shows that staffing trends are holding steady, although the four week moving average is 11.5% lower year-over-year. We follow temporary staffing levels because short-term staffing changes typically occur before changes in full-time staffing. So far this cycle, temporary staffing has shown more weakness than unemployment insurance claims, nonfarm payrolls, and unemployment.

The NAHB/Wells Fargo Housing Market Index (HMI) rose two points to 41 in September, breaking a four month decline in the survey. Readings above 50 are indicative of favorable single-family home builder sentiment. “Thanks to lower interest rates, builders now have a positive view for future new home sales for the first time since May 2024”, according to NAHB Chair Harris. The current sales conditions index rose one point to 45, the measure of sales expectations over the next six months increased four points to 53, and the prospective buyer traffic index increased two points to 27. Regionally, the Northeast was the strongest, despite falling three points to 49, and the West remained the weakest after rising one point to 39. The Midwest rose one point to 40 and the South dropped one point to 41.

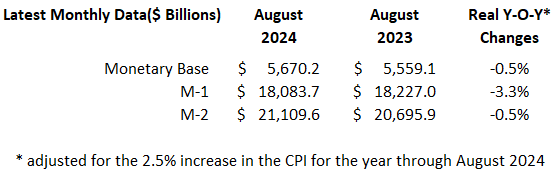

MONEY SUPPLY

Below is the monthly update of the Marketimer and Brinker Fixed Income Advisor Model Portfolios through September 30, 2024.