Model Portfolios | September Update

S&P 500 6460.26 | 10-Year UST Yield 4.23% | September 1, 2025

“It is sheer madness to live in want in order to be wealthy when you die.”

-Juvenal

COMMENTARY

The S&P 500 Index reached new all-time highs on several occasions in August and has surpassed our target of the low 6,000s. The highest close was achieved on August 28th at 6501.86. The index has increased roughly 5% from its February closing highs. The resilience of the current bull market, which began in October 2022, has been impressive. The S&P 500 currently trades at 24.4 times its current-year earnings estimate of $265.

The Conference Board Leading Economic Index (LEI) fell 0.1% in July, after a 0.3% decline in June. Over the six-month period ending in July 2025, the LEI fell 2.7%, versus the 1.0% decline seen in the prior six months. “The Conference Board does not currently project a recession, though we do expect the economy to weaken in H2 2025, as the negative impacts from tariffs become more visible. Overall, real GDP is projected to grow by 1.6% year-over-year in 2025, before slowing in 2026 to 1.3%.”

Real GDP growth averaged 1.4% during the first half of 2025. The most recent Atlanta Fed GDPNow model forecasts 3.5% real GDP growth in the third quarter, while the New York Fed GDP Nowcast anticipates 2.2% growth.

HOUSING MARKET UPDATE

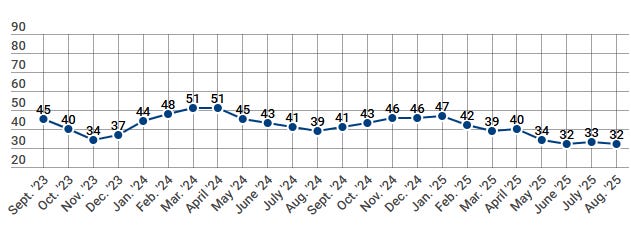

The NAHB/Wells Fargo Housing Market Index (HMI) measures conditions in the single-family housing market. The HMI index fell one point to 32 in August, returning the index to its lowest level in recent years. HMI Index readings above 50 indicate favorable sentiment among single-family home builders. The current sales conditions index fell one point to 35. The measure of sales expectations over the next six months remained unchanged at 43, and the prospective buyer traffic index increased 2 points to 22. Regionally, the Northeast was the strongest, falling one point to 44. The Midwest rose one point to 42. The South fell one point to 29, and the West was the weakest, declining one point to 24.

INFLATION UPDATE

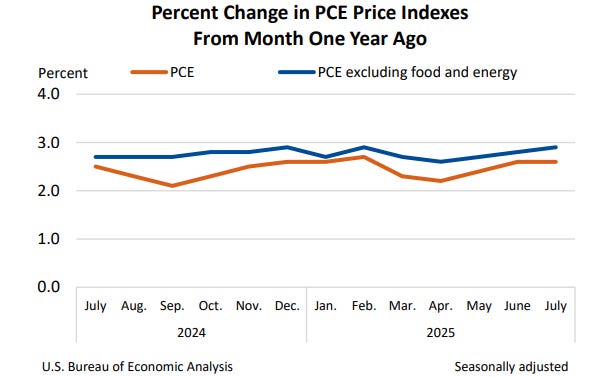

The Fed’s preferred inflation measure is the personal consumption expenditure (PCE) price index. The most recent PCE report showed that the index increased by 0.2% in July. The core PCE, which excludes the food and energy components, rose 0.3% in July. On a year-over-year basis, headline PCE increased 2.6% and core-PCE increased 2.9% in July.

As shown in the chart below, the headline and core PCE rates have been trending sideways for over a year. The most recent three-month annualized headline PCE inflation rate is 2.6%, and the three-month annualized core-PCE rate is 3.0%. The upcoming September FOMC meeting may be one of the rare occasions when the FOMC lowers the fed funds rate, despite three, six, and twelve month core inflation running above the Fed’s 2% target. We anticipate that the weakening labor market will be used as justification for a rate cut in September.

Headline PCE:

+0.2% seasonally adjusted in July, following 0.3% in June

+2.6% year-over-year

+2.6% latest 3 months annualized

+2.5% latest 6 months annualized

Core PCE: (excludes food and energy)

+0.3% seasonally adjusted in July, following 0.2% in June

+2.9% year-over-year

+3.0% latest 3 months annualized

+3.0% latest 6 months annualized

FEDERAL RESERVE UPDATE

The next Federal Open Market Committee (FOMC) Meeting is scheduled for September 16th and 17th. A 25 basis point rate cut at the September FOMC is likely. The meeting will include an updated Summary of Economic Projections (SEP) from FOMC members. Here is a link to their most recent June 2025 projections. The SEP’s year-end 2025 federal funds rate projection is within the 3.9% to 4.4% range.

CME FedWatch shows an 87% probability of a 25-basis-point rate cut at the September FOMC meeting, with the potential for one additional rate cut in October.

Fed Chair Powell’s four-year term as Fed Chair is set to expire in May 2026. The current favorite to replace him is Fed Governor Christopher Waller, though that may change over the coming months. Fed Governor Kugler resigned in August, opening one spot on the seven-member Board of Governors. Kugler’s term was set to expire in January 2026. President Trump nominated Stephen Miran to fill the vacancy created by Kugler’s unexpected resignation. President Trump and Fed Governor Cook are engaged in a legal dispute to determine whether she will remain on the Board of Governors.

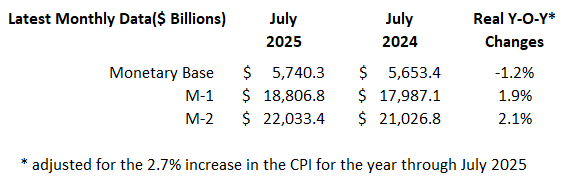

MONEY SUPPLY

MODEL PORTFOLIOS UPDATE

Below is the monthly update of the Marketimer and Brinker Fixed Income Advisor Model Portfolios through August 31, 2025.