Gross Domestic Product + Inflation Update

Third quarter real GDP +4.9%. Headline PCE inflation +3.4% and core PCE inflation +3.7% in September.

GROSS DOMESTIC PRODUCT (GDP)

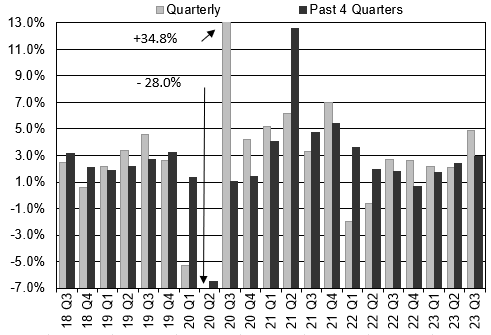

Real gross domestic product (GDP) increased at a 4.9% annual rate in the third quarter of 2023, following 2.1% real GDP growth in the second quarter and 2.2% in the first quarter. Through the first three quarters of 2023, real GDP growth averaged 3.1%, above our 2.0% long-term trend growth estimate for the U.S. economy.

Personal consumption expenditures (consumer spending) are the most important component within the GDP report, representing nearly 70% of GDP. During the third quarter, PCEs contributed 2.7% to the overall 4.9% GDP figure, up from a 0.55% contribution in the second quarter. Gross private investment contributed 1.5%. Net exports subtracted -0.1% and government consumption expenditures added 0.8%. You can view a more detailed real GDP contribution breakdown in Table 2 of the report.

The Atlanta Fed GDPNow does a respectable job of forecasting current quarter GDP as the data becomes available. GDPNow’s initial estimate of fourth quarter real GDP (using limited data) is for real GDP growth of 2.3%. The accuracy of the GDPNow figure improves throughout the quarter as more data is published.

INFLATION UPDATE

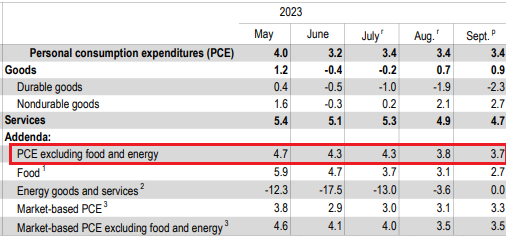

The PCE inflation report showed the PCE price index increased 0.4% during September. The core PCE, which excludes the food and energy components, rose 0.3% during the month.

The pace of headline PCE inflation peaked at 7.1% year-over-year in June 2022 and has decelerated to 3.4% recently. The core PCE rate, which excludes food and energy prices, peaked at 5.6% in February 2022 and has decelerated to 3.7% in September 2023. The deceleration in the headline PCE rate has leveled off recently, with the July, August, and September year-over-year inflation rates holding at 3.4%.

Although the headline and core inflation rate remain above the Fed’s 2% target level, we expect the Fed will hold the fed funds rate steady at the current 5.25% to 5.5% target level at next week’s FOMC meeting. Looking beyond next week to the December FOMC meeting, the probability of another rate hike this year has fallen to less than 20%.

Headline PCE:

+0.4% seasonally adjusted in September, following +0.4% in August

+3.4% year-over-year

+3.8% latest 3 months annualized

+3.1% latest 6 months annualized

Core PCE: (excludes food and energy)

+0.3% seasonally adjusted in September, following +0.1% in August

+3.7% year-over-year

+2.5% latest 3 months annualized

+2.8% latest 6 months annualized

Long-Term Chart of Headline and Core PCE Inflation (Year over Year Change)

Summary Tables from BEA.gov PCE report:

Core-PCE YoY Percent change from the same month one year ago:

Source: BEA.gov

U.S. TREASURIES + CD DEALS

Next week includes attractive U.S. Treasury auctions including 3-month, 6-month, and 12-month bills. These maturities currently yield between 5.4% and 5.6%. Treasuries are especially attractive for investors in regions with high state income taxes.

Barclay’s bank is offering attractive CD selections with APY’s between 5.0% and 5.5% on 12-month, 18-month, and 24-month CDs.

NexBank also has some attractive CD offers:

Finally, PopularDirect has these CD rates available:

Stay tuned for our next post after the November 1st FOMC meeting next week that will include the Marketimer and the Brinker Fixed Income Advisor Model Portfolio performance through October 2023.

We will also post an update on the Series I Savings Bond soon.

This post is free to read, so please share it with anyone you think may benefit.