Model Portfolios | April Update

S&P 500 5254.35 10-Year UST Yield 4.20% :: March 31, 2024

“It's a wonderful thing to be optimistic. It keeps you healthy and it keeps you resilient.”

COMMENTARY

The S&P 500 closed out the first quarter of 2024 at an all-time record high on March 28th at 5,254.35. The index rose 3.1% during the month of March and 10.2% during the first quarter. Since bottoming in late October 2023, the S&P 500 has increased 27.6% in just over five months, an impressive feat. If we look back to the October 2022 closing low, the S&P 500 has risen 46.9% during the current bull market.

The NAHB/Wells Fargo Housing Market Index (HMI) rose three points to 51 in March, its fourth consecutive monthly increase. Readings above 50 are indicative of favorable single-family home builder sentiment. This was the first reading over 50 since July 2023. The current sales conditions index rose four points to 56, the measure of sales expectations over the next six months increased two points to 62, and the prospective buyer traffic index rose two points to 34. The NAHB Chief Economist noted that “as home building activity picks up, builders will likely grapple with rising material prices, particularly for lumber.”.

INFLATION UPDATE

The personal consumption expenditure (PCE) inflation report showed the PCE price index increased 0.3% in February. The core PCE, which excludes the food and energy components, also rose 0.3% during the month.

The pace of headline PCE inflation peaked at 7.1% year-over-year in June 2022 and has decelerated to 2.45%. The core PCE rate peaked at 5.6% in February 2022 and has decelerated to 2.8%. Both the three-month headline PCE inflation rate and the three-month core-PCE inflation rate rebounded higher in February. The three-month headline PCE annualized rate rose from 1.98% to 3.39% and the three-month core-PCE annualized rate increased from 2.81% to 3.52%. This is not the inflation data FOMC members hoped to see; as a result, prospective rate cuts are being pushed out at least a meeting or two. It is unlikely that most FOMC members will feel comfortable cutting the fed funds rate as long as the three-month headline and core PCE inflation rates are above 3.0%.

Headline PCE:

+0.3% seasonally adjusted in February, following 0.4% in January

+2.5% year-over-year

+3.4% latest 3 months annualized

+2.5% latest 6 months annualized

Core PCE: (excludes food and energy)

+0.3% seasonally adjusted in February, following +0.5% in January

+2.8% year-over-year

+3.5% latest 3 months annualized

+2.9% latest 6 months annualized

FEDERAL RESERVE UPDATE

The next FOMC Meeting is scheduled for April 30th and May 1st. In case you missed it, here is our update published last week following the March FOMC meeting, which included a revised Summary of Economic Projections. We do not anticipate any monetary policy change at the April 30th/May 1st FOMC meeting.

Last week, Fed Governor Waller gave an excellent speech titled “There’s Still No Rush,” emphasizing that the Fed has plenty of time to digest the incoming inflation data before lowering the fed funds rate.

I continue to believe that further progress will make it appropriate for the FOMC to begin reducing the target range for the federal funds rate this year. But until that progress materializes, I am not ready to take that step. Fortunately, the strength of the U.S. economy and resilience of the labor market mean the risk of waiting a little longer to ease policy is small and significantly lower than acting too soon and possibly squandering our progress on inflation.

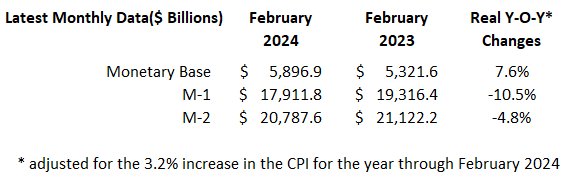

MONEY SUPPLY

Below is the monthly update of the Marketimer Model Portfolios and the Brinker Fixed Income Advisor Model Portfolios through March 31, 2024.