FOMC Meeting and LEI Update

"Strive not to be a success, but rather to be of value." -Albert Einstein

FEDERAL OPEN MARKET COMMITTEE | SEPTEMBER 2024

The Federal Open Market Committee (FOMC) held a two-day meeting on September 17th and 18th. FOMC members voted 11-1 to lower the federal funds rate by 50 basis points (one-half percent) to the 4.75% to 5.0% target range and to continue the quantitative tightening program that reduces the Fed’s balance sheet at a pace of up to $60 billion per month. Fed Governor Bowman voted against the policy decision in favor of a smaller 25 basis point rate cut. Below is the post-meeting FOMC statement:

Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have slowed, and the unemployment rate has moved up but remains low. Inflation has made further progress toward the Committee's 2 percent objective but remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee has gained greater confidence that inflation is moving sustainably toward 2 percent, and judges that the risks to achieving its employment and inflation goals are roughly in balance. The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

In light of the progress on inflation and the balance of risks, the Committee decided to lower the target range for the federal funds rate by 1/2 percentage point to 4-3/4 to 5 percent. In considering additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Michael S. Barr; Raphael W. Bostic; Lisa D. Cook; Mary C. Daly; Beth M. Hammack; Philip N. Jefferson; Adriana D. Kugler; and Christopher J. Waller. Voting against this action was Michelle W. Bowman, who preferred to lower the target range for the federal funds rate by 1/4 percentage point at this meeting.

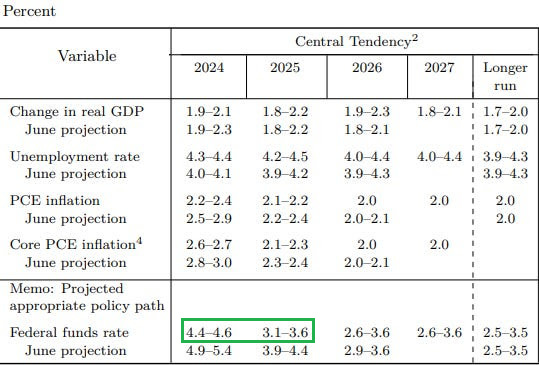

The September FOMC meeting allowed committee members to share their latest economic projections. The table below shows the latest figures and the prior (June) figures using the projections’ central tendency, which excludes the three highest and three lowest projections for each variable each year. The forecast for 2024 and 2025 real GDP growth is mostly unchanged near the 2.0% trend growth rate. The unemployment rate projection is slightly higher near the current 4.2% level, and the inflation rate is a bit lower and very close to the 2.0% inflation target. The federal funds rate projection for year-end 2024 is a range of 4.4% to 4.6%, which implies two additional 25 basis point rate cuts are anticipated at the two remaining FOMC meetings this year in November and December. As we wrote last week, the opportunity to earn a 5% risk-free return is ending.

The “dot plot” below shows each FOMC member’s fed funds rate forecast for December 2024, December 2025, December 2026, and over the long term. As you can see, all but two FOMC members anticipate at least one more 25 basis point rate cut this year, and nearly all FOMC members forecast a federal funds rate that will decrease to within a range of 3.0% to 3.75% over the next fifteen months. The takeaway from the dot plot is simple: FOMC members expect a series of rate cuts over the coming quarters that will lower the fed funds rate by roughly 2% from its recent peak.

Below is a video and transcript of Fed Chair Powell’s media conference:

LEADING ECONOMIC INDICATORS | AUGUST 2024

The Conference Board Leading Economic Index® (LEI) decreased by 0.2% in August, following a 0.6% decline in July. During the six-month period ending in August, the LEI contracted by 2.3%, slightly better than the 2.7% decline observed in the previous six-month period. Current GDP growth projections for the third quarter of 2024 look good, with the Atlanta Fed's GDPNow model estimating 2.9% real GDP growth and the New York Fed's Nowcast estimating 3.0% third-quarter growth.

“Overall, the LEI continued to signal headwinds to economic growth ahead. The Conference Board expects US real GDP growth to lose momentum in the second half of this year as higher prices, elevated interest rates, and mounting debt erode domestic demand. However, in the Fed’s September 2024 Summary of Economic Projections, policymakers suggested 100 basis points of interest rate cuts are likely by the end of this year, which should lower borrowing costs and support stronger economic activity in 2025.”

-Justyna Zabinska-La Monica, Senior Manager, Business Cycle Indicators, at The Conference Board

Source: The Conference Board

The Coincident Economic Index® (CEI), which gauges present economic conditions, rose 0.3% in August, following a 0.1% decline in July. During the six-month period through August, the CEI rose 0.8%, slightly faster than the 0.6% growth rate observed in the previous six months. All four CEI components increased in August.

In case you missed it, last week we posted our favorite money market and CD rates. We think the tax-equivalent yield offered in municipal money market funds is attractive for investors in the highest federal income tax brackets holding cash in taxable accounts.

Our Model Portfolio Update for October 2024 is scheduled to be published on October 1st. Here is our most recent September Model Portfolio Update.